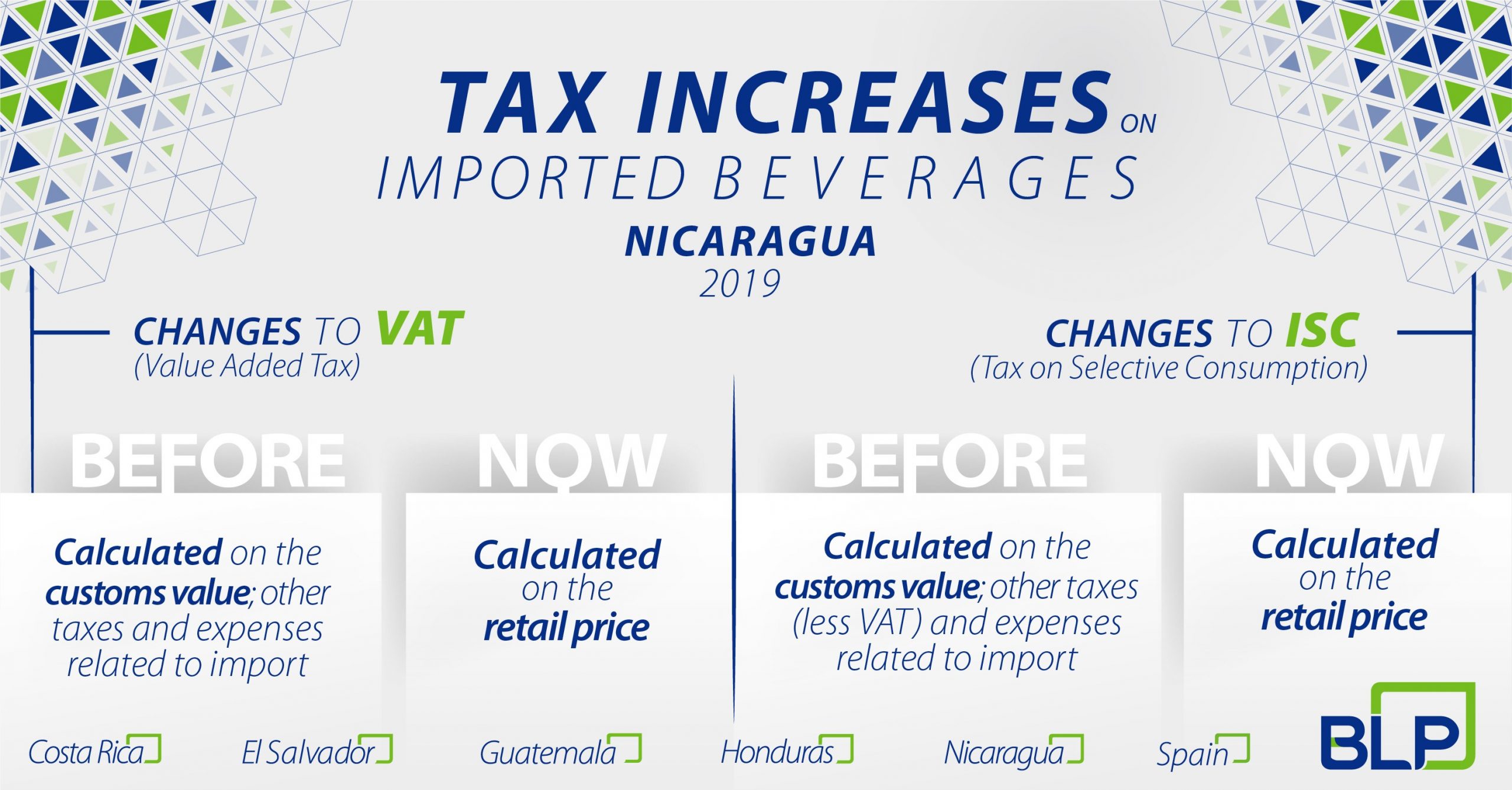

Due to the reform of the Tax Agreement Law published on February 28, 2019, the tax burden on the importation of juices, soft drinks, and energy drinks increased both in the Value Added Tax (VAT) and in the Selective Consumption Tax (ISC):

a) Value Added Tax

- Previously the tax was calculated on the customs value plus other taxes and expenses related to importation; now it is calculated on the price to the retailer.

b) Selective Consumption Tax

- Basis of calculation of the tax was the customs value plus other expenses and taxes related to importation (minus VAT), but now it is calculated on the price to the retailer.

- Increase in the tax rates on imports.

In both cases, the amendment to the Regulation of the Tax Agreement Law establishes that the price to the retailer on which the tax will now be calculated will be established by the National Development Information Institute (INIDE) who will communicate it quarterly to the Customs Office. To date, communication in this regard by the INIDE has not been made public, which means that the requirement to allow the tax to be applied is not met since there is no way to calculate it legally.

Therefore, any retail price determined by an authority other than the one established in the Regulation, including the Customs Administration itself, is unlawful, due to constitutional limitations that prevent public officials from exercising functions other than those granted by the legal system. As a result, the charges reported by importers on this type of beverage in which three times the CIF value of the merchandise is used as a tax base are illegal.

The demand of the sector is that INIDE establish the prices to the retailer and that said prices are communicated through a technical circular of the Customs Administration so that they can calculate prior to importation the tax burden to which the operation would be subject, thus guaranteeing the respect for legality and providing legal security. In addition, importers denounce the existence of retroactive charges on goods imported prior to the application of the new tax rates. In this sense, it is important to highlight that the Political Constitution prohibits the retroactivity of the law, except in specific cases. Therefore, the Customs Administration may begin to collect the tax with this new tax base only from the date of the INIDE pronouncement.

However, it is also relevant to mention that since the tax reform came into force it is illegal to continue calculating the tax based on the previous calculation because that calculation method is no longer valid. This does not mean that the goods are exempt, but as long as the absence of a determination of the tax base lasts, it is impossible to calculate the tax.

In conclusion, a prompt solution is urgently needed. The current situation is detrimental to international trade operations and affects not only importers but also the rest of the players in the marketing chain until it reaches the final consumer. Because it is impossible to determine the taxes payable for import operations, product shortages are possible, along with an economic shortfall to the Customs Administration itself.

For more information contact: [email protected]

BLP